"But the worst part isn’t the being rendered naked and defenseless before the robbers. It is that the robbers will be able to tell you what you may – and may not – do with whatever they leave you after they rob you."

Authored by Eric Peters via EricPetersAutos.com,

The “Federal” Reserve – in the usual air-finger-quotes, to emphasize the maliciously disingenuous verbiage, the “Fed” being a conglomeration of private banks that controls the federal government and so, practically everything else, via the issuing of money it creates out of nothing that it loans at interest to the federal government – has up to now been a kind of background evil. Few knew about or understood its machinations – its manipulations – because few had any direct dealings with it.

It was just, you know, the “Fed.”

That is about to change.

Come July, the Fed will involve itself directly in the affairs of Americans, via Fed Now – a chirpily named etiolation of the “Fed’s” manipulation of the nation’s money supply. The object now isn’t manipulation as much as it is habituation.

To “federal” control over what you are allowed to buy and sell with the digital money it controls. FedNow is the Beta version of what is meant to become the Fed’s Central Bank Digital Currency (CBDC). It is just a matter of getting people used to it. As they got used to wearing Face Diapers. To being fondled as a condition of travel. To election months rather than election day. And so many other such things. All in good time, my pretty, the wicked witch says.

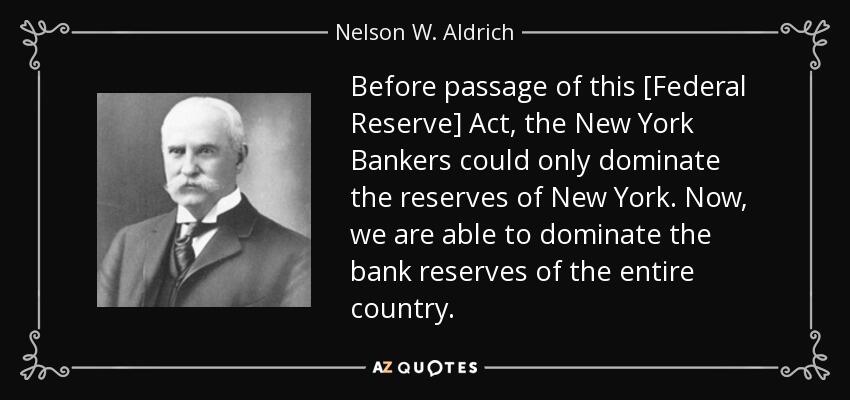

As things have stood since the creation of the “Fed” by the private banks – by the rich men that controlled those banks – using their riches to buy politicians such as Nelson Aldrich (whose daughter married a Rockefeller, who gave birth to politician Nelson Aldrich Rockefeller) the “fed” has controlled the economy via its control of the money used by the economy.

It has used what is styled “inflation” to devalue the buying power of money and so egg-on people to spend it before it buys less. This discourages savings and rewards profligacy, which profits the “Fed” and those close to it via the encouraging of debt-based living, upon which the banks and related institutions feed, via the interest they collect. The end result is a society in which the banks own almost everything that matters, while most people pay interest on debt most of their lives, many of them ending their lives with little to show for it.

But impoverishing people by eroding their wealth and keeping them chained to debt is only a partial solution as there are still people who find a way to live within their means, avoid debt and – worst of all – avoid being controlled. They are the people who aren’t wage slaves, who deal in cash, anonymously – and by dint of that, avoid what are styled “taxes,” the legalized robbery committed by the government that is the tag-team enserfer of the American people, along with “inflation.” If money retained its buying power – if it were not made of paper – and if people weren’t robbed of their money – most people would have money enough to live comfortably and, most of all, they would be largely immune to much of the bullying so many currently endure at the hands of the government-corporate nexus.

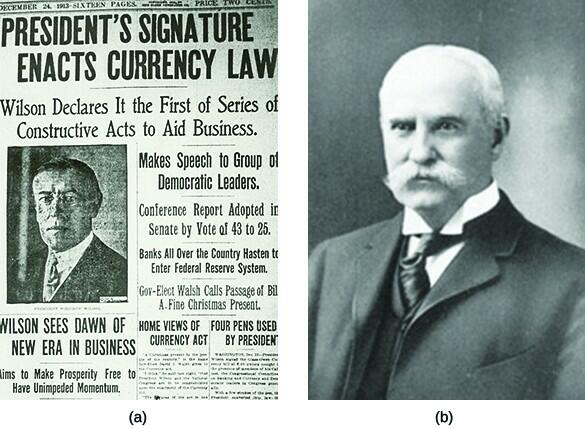

The “Fed” being one of the first mergers of the two when it was created back in 1913 – courtesy of the services rendered by bought-and-paid-for politicians such as Senator Nelson Aldrich. The latter was also instrumental – uncoincidentally – in the passage of the 16th Amendment, which legalized the federal income tax. So as to assure the people would be robbed of their money when they earned it as well as their money robbed of its value when they spent (or tried to save) it.

Now the nexus wants to assure that people who have managed to escape these forms of control will be placed under control – by making it so that every transaction they make is known – or put another way, they will make it impossible for anyone to make any transaction without it being known.

And subject to approval as well as immediate robbery.

The “Fed” – which is to say, the nexus – would know every last detail of your financial life, down to the can of soda you just bought – using their app in lieu of cash. You will pay every cent of what they say you “owe” in taxes. The good news is it will probably no longer be necessary to file taxes every April. The bad news is you’ll be paying taxes – all of them – all year long. No more under-the-table cash transactions, the latter imputed with disreputability – as if it were disreputable to hide one’s money from those who would rob one of it.

But the worst part isn’t the being rendered naked and defenseless before the robbers. It is that the robbers will be able to tell you what you may – and may not – do with whatever they leave you after they rob you.

When they can prevent you from buying, you will only be able to buy with their permission. Which will only be granted if you are obedient. Easy – instantaneously – when money becomes a digitized app, the app under their control

The main reason the “pandemic” didn’t achieve its ends entirely was that millions were able to ignore it and go about their lives – and their business. Especially those who operated outside of the grasp of the nexus, being self-employed or self-sufficient. They could buy food; they could buy fuel. Thus, they were able to say a stalwart No to face diapers and the drugs pushed by the nexus. They are still able to not buy an EV – and drive an SUV – to and from their single family home, which isn’t an apartment in a 15 Minute City.

It will be much harder to say No – to anything – when the nexus can say No, to them.

Attention, citizen! There is a climate lockdown in effect. Shelter in place. Await instructions.

Or else.

This is what FedNow is all about. Not immediately, of course. But piece-by-piece. Just as the income tax was only paid – at first – by the “rich.” Who of course didn’t pay it, being rich enough to pay politicians to enact exemptions and “write-offs” so as to ameliorate the burden, which was quickly passed on to the middle and working classes, who could not afford to buy politicians.

FedNow is presented as innocuous and even helpful. Instantaneous transfer of money! Avoid those late fees! Pay at the very last second, anytime you like!

“FedNow is the Federal Reserve’s new instant payment service that will enable customers at participating banks and credit unions to send and receive money within seconds, 24/7 and every day. You’d be able to complete payments or transfers on weekends, holidays and after banks’ business hours.”

The head of the “Fed” – Jerome Powell – says “What FedNow will do is it will enable all the banks, any bank in the United States — not just the big ones — to offer instantly available funds and real-time payments to their customers.”

And many other things besides.

This is poison. Cancer. We will not survive it if it is not excised, then burned and the ashes scattered to the winds. The nexus intends to “launch” FedNow in July. If we do not wish to be controlled – utterly and implacably and forever – this “launch” must be met with resistance. This option is still available to us – in the form of not having anything to do with it. Or the banks that are involved with it.

No is an immensely powerful weapon. If only people would learn to use it.

No comments:

Post a Comment